Table of Contents

What is an insurance broker?

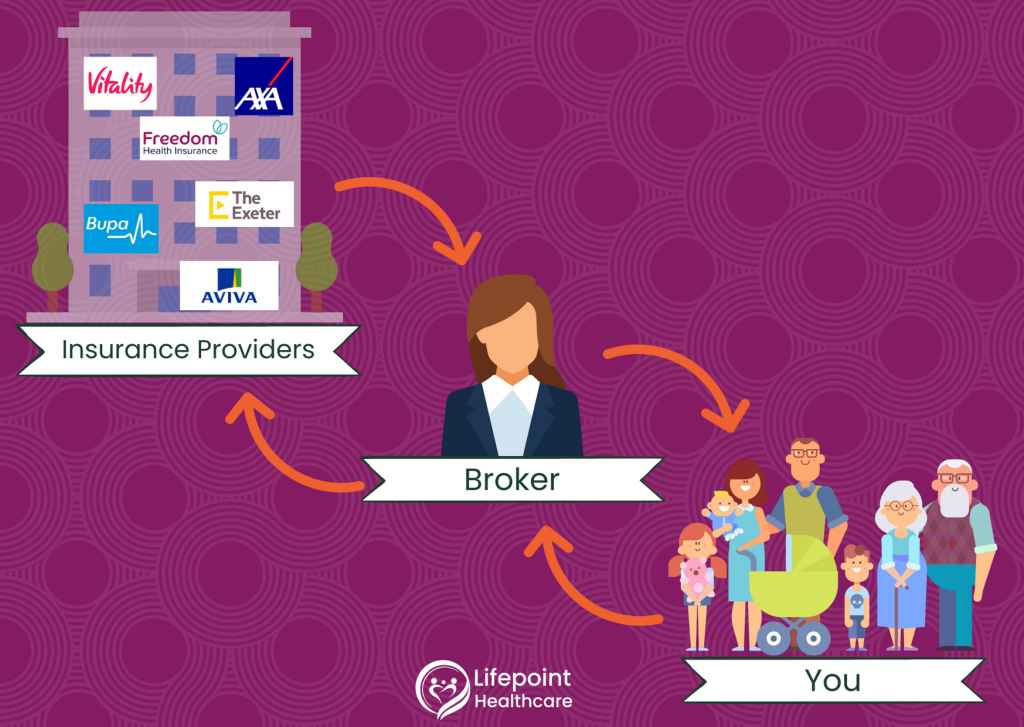

An insurance broker is an intermediary between the big, faceless, corporate insurance providers and you, the consumer. They help to simplify the complex world of private medical insurance and possess extensive knowledge and expertise about insurance policies and companies. As a result, they can offer you informed, valuable and objective advice.

Some insurance brokers offer more general advice and cover a wide range of types of insurances, whilst others offer advice within a more narrow niche. For example, Lifepoint Healthcare only offers insurance advice on private medical insurance. Brokers that operate within a niche can often offer more in-depth and personalised advice than more general operators.

An insurance broker will help people and companies to find the right coverage for their needs. They listen to your needs and requirements and do the leg work for you, shopping around various insurance providers in order to offer you the most suitable policy.

Brokers are independent operators and work for you, not the insurance providers. As a result, they can afford to be honest and impartial in the advice they offer.

Insurance brokers usually help with more than just the initial policy setup. They use their knowledge to break down confusing insurance jargon into easy-to-understand language so you can get to know your policy in more detail. They can also help with paperwork so you get your cover arranged with no delays and help you if you need to make a claim.

Myth Buster

It’s a common misconception that it will cost you more to use an insurance broker but in fact, the opposite is true. Their services are normally free to you, and they can often save you money on the policy itself. To find out more about how brokers get paid, keep reading!

How Brokers Get Paid

Despite a common misconception, insurance brokers are not paid by you.

Brokers make their money on a commission basis from the insurance companies. Insurance companies will remunerate the broker for the referral, usually as a percentage of the policy cost.

The insurance companies get your business, the broker receives a commission and you get free advice and the best policy to fit your needs. Everybody wins!

It is important to note that the premium does not increase by using a broker and your premiums are, in most cases, the same if you go directly to an insurer.

Brokers Vs Tied Agents

You might be wondering if the broker is incentivised to pass your business on to one specific insurer. The answer is no – what you’re thinking of is a tied agent.

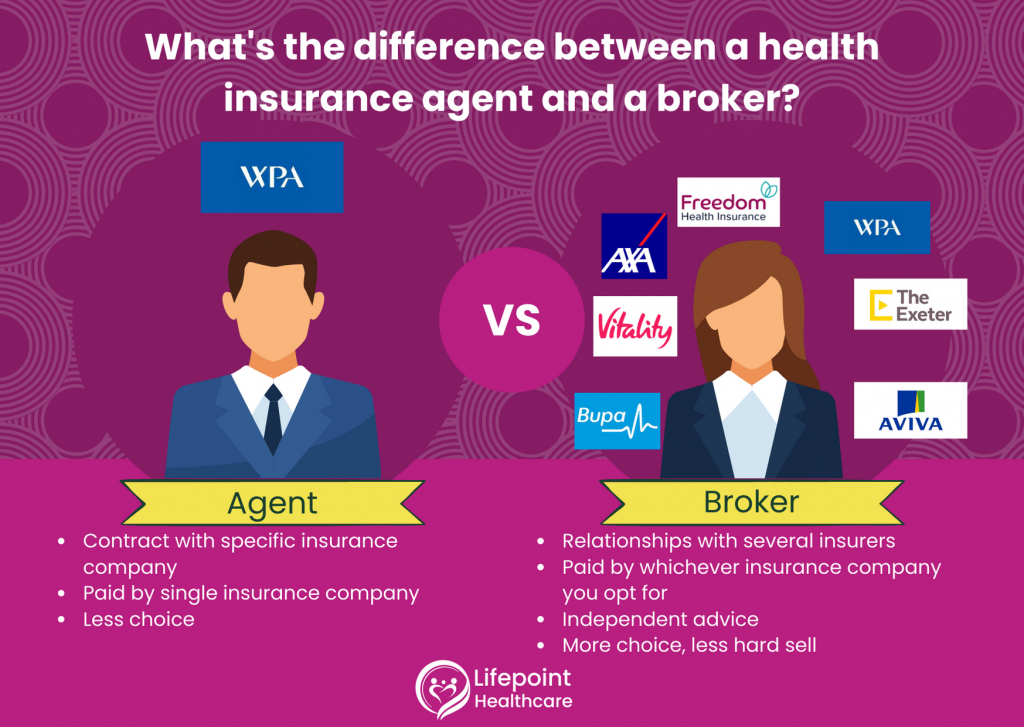

It’s a common assumption that “agent” and “broker” are just different names for the same thing. Though there are some similarities, there are also crucial differences.

A tied agent works directly for a specific health insurance company, for example – XYZ Insurance Company (not a real company!). As a result, they can only give you options within the scope of what XYZ Insurance Company can provide, with no consideration for other insurance providers. They are paid by the company they sell for.

A health insurance broker acts independently and usually works with a variety of health insurance providers. They can often also offer you insurance provided by XYZ Insurance Company, but also insurance provided by a whole host of others.

The result is more options for you and less of a hard sell approach as they will get remunerated by whichever health insurance provider you opt for.

What to look for in a health insurance broker

There are a number of ways to evaluate the trustworthiness of your private health insurance broker.

Things to look for:

- Brokers need to be authorised and regulated by the FCA. Always check the firm you are dealing with is listed on the Register. Details can be checked on the register here

- Though not mandatory, it might be a comfort to you if your broker has industry qualifications called the IF7 exam. This ensures that they are committed to their professional reputation and development.

- Another sign of legitimacy is a broker who is a member of the AMII – the Association of Medical Insurers and Intermediaries. Though it isn’t mandatory, it is certainly a good sign. The AMII is a trade association for independent medical insurance advisors in the UK and was established in 1998. It now has more than 120 professional intermediaries.

- Another great way to check a broker’s reliability is to use online social proof. Google reviews are a great place to start – Do they only have a few reviews? What’s the five-star average? Are their customers raving fans or ambiguous? Their website is another key indicator – Is it up to date? Is it professional?

- Your broker should be easy to communicate with! After all, you want to know you can get hold of them if you need help making a claim. Some great questions to ask yourself are: Is it easy to get hold of a real person? Are they helpful and communicative? Are they reliable in their communications and deadlines?

Red flags:

- A broker should have an in-depth understanding of private medical insurance – if they seem unsure or like they’re winging it, beware!

- A lack of communication – if they are difficult to get hold of or do not return calls promptly, consider that they might not be there to answer your questions when you really need them!

What to expect when working with a health insurance broker

When you first get in touch with a broker, there will be a series of steps. Though procedures may vary slightly between brokerages, the general process is the same.

1. Fact find

When you talk to a health insurance broker, you should start with a relaxed, yet thorough conversation to gather the facts, assess your needs, and help you determine how health insurance best supports your goals. It’s critical that any broker you engage with listens to your needs, and helps you understand the options available.

They may ask you questions such as:

- Is this your first time buying health insurance?

- What’s prompted your enquiry at this point in time?

- If you already have coverage, why do you want to review or switch?

- How often do you currently go to the doctor and do you see any specialists?

- Have you had any treatment or consultations in the past 12 months?

- Do you have any tests, investigations or treatments planned or pending?

- What is your budget?

- Is the policy for you, you and your partner, you and your family or you and your company?

2. Going to market

Your broker will then go away and complete a fair and objective analysis of the market by comparing products from a wide range of insurers. They will base their search on your specific requirements, taking into consideration your goals, needs and budget.

Usually, several suitable opinions are presented to you at this stage. They will present findings in a clear and comprehensible way and ensure that you understand all your options, the advantages and disadvantages of each plan, as well as offering a clear recommendation. Together with your broker, you can decide on your perfect fit.

3. Selecting a plan

Once you have decided on a plan, your broker will go through the details with you. This ensures that you know your policy inside out. The broker will also help you with paperwork and arranging the payment on the policy.

It’s important to note that most health insurance brokers do not handle the payments for policies, so they will direct you to your new insurer for payment options.

Your broker should continue to provide care and support throughout the life of your health insurance policy. As long as you are a customer, you should have direct access to your broker or an informed member of the team who can quickly and simply answer your queries that may arise over the course of your policy.

How brokers can help you

Brokers can be useful regardless of your current private health insurance situation. Here are some ways they can help:

- Find a new policy – Whether you’re a first-time buyer or have previously had private medical insurance.

- Review your current policy – They can help ensure that your current cover is cost-effective and fit for your needs. Though this is often done annually, they can assist in between these dates too.

- Switch policies – They can assist you if you want to replace an existing policy, whilst ensuring that you keep all the cover you need.

Benefits of using a health insurance broker

The benefits of using a health insurance broker over attempting to go it alone are numerous. Let’s get stuck in!

1. Cost Savings

Since the services of a broker are free, and they can usually negotiate better prices for the same cover than the average customer can, it goes without saying that you will probably save money!

2. Objective Risk Assessment

One of the biggest bonuses of using a health insurance broker in the UK is the extensive knowledge they possess surrounding the UK’s private healthcare system. They can help you make risk assessments, on both policy and financial decisions, with the knowledge built over years in the industry. This experience is not to be underestimated!

3. Honest Advice

Health insurance brokers in the UK don’t usually have any affiliations to insurance providers so they can offer you honest opinions about what works for you.

At Lifepoint Healthcare, our team is always honest with the customer – even if that means that you don’t purchase private health insurance.

4. Simplified Communications

A good broker will break down discussions about policy and coverage into a language you understand. It’s easy to get bombarded with facts when dealing with insurance companies but a broker can give you good, easy to understand, jargon-free advice to keep you feeling relaxed and in control.

5. Range of insurer options

Brokers work with a variety of private health insurance providers in the UK. This means that you will get to choose easily between multiple providers to find your perfect fit.

6. Accurate policy comparisons

Ok, we’re just going to say it. Reading health insurance policies isn’t the most gripping activity in the world.

It can be tricky for most people to see the nuances and differences between policies that all look the same on the surface. With their extensive knowledge of the products, system and industry, brokers can summarise and simplify each policy so you can see your options easily!

7. Negotiating premiums

Brokers have working relationships with insurance companies and help them to get more people on their books. As a result, trust is built up in the relationship.

You get to benefit directly from this trust and brokers can often negotiate a more competitive price than you would be able to as a standalone customer.

8. Time-saving

Probably the biggest benefit of using a health insurance broker for busy, working people is how much time can be saved.

Trawling through insurance providers sites, trying to teach yourself the ins and outs of the industry and talking to agents and salespeople can be exhausting. Nobody wants to spend their weekend doing that.

With a broker, you only have one simple conversation and the rest is taken care of for you.

In a world that is leaning increasingly towards the “work smarter, not harder” mentality, going with a broker is a no-brainer!

9. Claim assistance

Like all insurance, we all hope we never have to use it. If you do have to make a claim on your health insurance, it will probably be a stressful and worrying time for you and your family. Brokers can help with claims assistance, walking you through the process and ensuring that you’re doing the right things.

10. Free service with no obligation to buy

Health insurance brokers in the UK normally work free of charge for you, the customer. Even after they have presented you with your health insurance quotes and advice, there is no obligation to make a purchase.

This makes it pretty much risk-free to chat to a broker. Book a call with our friendly team of advisors now!

Going it alone

Despite the many benefits of working with a health insurance broker, many people may still wish to go it alone.

If you’re going to go solo when purchasing your first private health insurance policy, we recommend talking to as many different insurers as possible.

Approach all the major players – Bupa, Aviva, Axa etc – as well as a few you may not have heard of. By approaching at least five insurers and giving yourself multiple options, you will begin to gain an understanding of the ballpark price and be able to find a suitable premium at a competitive price.

Another big tip is to take the time to understand what they are offering you. Set aside the time to get acquainted with private health insurance and make sure you know the essentials before even approaching insurance companies!

Conclusion

The world of private health insurance in the UK can be complex and confusing. Introducing a trustworthy, independent broker into the mix will save you time and money. They can also provide invaluable, objective advice and help you get the most out of your policy.

A good broker will make a sometimes stressful purchase feel calm and peaceful.