Growing old will, hopefully, happen to us all. One of the natural side effects of ageing is that we tend to experience more health issues. Over 50s health insurance allows access to private healthcare that will help deal with these health issues swiftly.

There is no practical difference between individual or joint policies for people over 50 versus people under 50. However, the cost of private medical insurance rises as we age. This makes it important to tailor the policy to minimise the price, without sacrificing too much cover.

What is health insurance for the over 50s?

Private medical insurance, or health insurance, allows the holder to access private healthcare. This means that they can use private hospitals, get to skip NHS waiting lists and get quicker access to treatment.

Private medical insurance covers the treatment of acute conditions, but not chronic conditions which might require long term management. Acute medical conditions include things like cancer, joint replacement surgery or pneumonia. Chronic conditions include things like high blood pressure, asthma and diabetes.

Private medical insurance often works in conjunction with the NHS, so having insurance does not prohibit you from using the health service.

Private medical insurance can be paid monthly or yearly and renews automatically each year unless it is cancelled. There are different types of policies available with various customisable elements, such as which hospitals you can use.

Is health insurance for the over 50s worth it?

Like all things, investing in health insurance when over 50 is about risk and reward. Most of us will experience more ill-health in our later years, which is why it could be the perfect time to take the plunge.

It is an inescapable fact that the cost of health insurance will rise as we age. This is due to the increased risk on the part of the insurance company – you are more likely to suffer from ill-health as you get older. If keeping costs low is a priority for you, private healthcare might not be the right move.

If the cost seems accessible for you, but you’re not sure if you need it… Well, then it’s a good idea to think about the potential benefits and see if it seems worth it.

The truth is that few people consider health insurance to be a priority – until you need it.

After all, we don’t plan to get ill or injured and according to AgeUK, 41% of adults admitted to hospital in 2017 were over the age of 65. Investing in health insurance while you’re healthy means that you are looking after the future you, in the worst-case scenarios.

It provides peace of mind, as well as a host of other perks, including:

- Prompt referrals to specialists – no lengthy NHS queues

- Treatment at a private hospital with a doctor of your choice and at a time that suits you

- Private hospital rooms, usually with ensuites, TVs, home comforts and often unrestricted visiting hours

- Access to treatments and drugs which are not always covered by the NHS

Though health insurance for the over 50s won’t meet all of your healthcare needs, such as chronic or pre-existing conditions, it will go a long way.

How much will over 50s health insurance cost?

The cost of your policy will depend on numerous factors. These include:

- Age (The cost rises incrementally with age)

- Where you live (e.g. If you live in London, the cost will be higher)

- Level of outpatient cover (The more extensive your cover, the more expensive it will be.

- Smoker status (If you smoke, or have smoked in the past, your cover will be more expensive)

- Medical history and current state of health (If you are in poor health, the cost may be more)

- Optional add-ons (See below)

- Your chosen hospital list. (Which hospitals you have opted to be treated at)

Some of these factors are outside of your control – like your medical history. Others, such as the level of outpatient cover and hospital lists, can be tweaked to bring the price down.

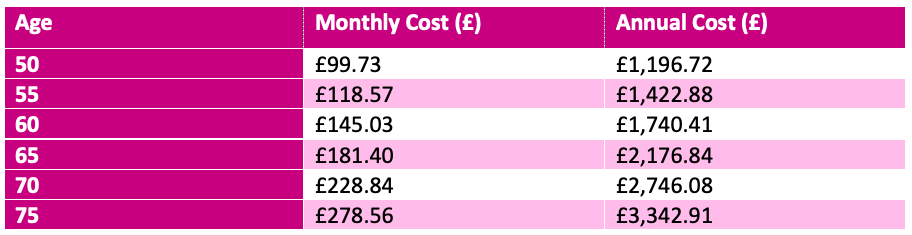

To give a ballpark figure of how much health insurance will cost, we have included some figures. These were generated from a popular price comparison site using the parameters: one person, non-smoker, outside of London, treatment and full diagnosis cover, no add-ons, is in good health, and would be willing to pay a £250 excess. The mean was taken of all of the prices to generate the average monthly cost which was multiplied by 12 to get the annual. These are accurate as of October 2021.

Please be aware that actual costs may vary!

Things to consider when buying over 50s health insurance

These points are all important to consider purchasing health insurance when you’re over 50…

But the most valuable piece of advice we can give is to find an experienced and impartial health insurance adviser, like Lifepoint Healthcare. They have in-depth knowledge to analyse your needs, wants and budget.

They also deal with you personally, rather than an automated website. This ensures that you understand fully what is going on at all stages of the process and won’t be stung by any nasty surprises further down the line.

Check out our blogs about the benefits of working with a health insurance broker!

Level of cover

When buying over 50s health insurance, there will be various levels of cover available, ranging from the most to the least comprehensive. The more treatments that are included, the higher the price of the policy. Treatments can be broken down into 3 categories:

Inpatient – This is included in all over 50s health insurance plans, even the most basic

Day-patient – This covered both overnight and non-overnight hospital visits where you need a bed, for example a minor surgery which required monitoring for several hours post-op, but not an overnight stay.

Outpatient – This covers all of the above, as well as the costs relating to treatments that do not require a hospital bed such as specific tests like MRI scans or blood tests.

There are multiple ways to ensure your policy is tailored to your needs and budget based on the above. For example, it is possible to include outpatient treatments up to a value of, for example, £1000 a year. This would mean that you could access these treatments without paying for unlimited cover.

Underwriting

There are several types of underwriting to choose from when purchasing over 50s health insurance. These are full medical underwriting, moratorium and switch. To learn more about underwriting, download our free ebooks.

Hospitals

The more hospitals where you can potentially receive treatment, the more expensive your policy will be. One easy way to save money if you don’t live in London is to exclude the London hospitals, which are the most expensive. If you keep your hospital list local to where you usually reside, the price will be further reduced.

Adding a 6-week NHS wait/deferment

This means that if the NHS waiting list for treatment is less than six weeks, the treatment will happen through the NHS. If it is more than six weeks, it will be private. This can help to reduce costs but obviously comes with the downside of potentially having to wait longer for treatment, which slightly defeats the point of having health insurance.

Excess

The excess is the amount of money you are willing to pay towards your own care.

The size of your excess will significantly affect your cover cost. If you’re happy to pay a larger excess, the overall cost of your policy will be lower. If you want a very low excess, your policy will cost more.

Optional add-ons

Add-ons to your policy allow you to personalise the features that you want to include. Some of these include:

- Psychiatric cover and complementary therapies

- Full cancer cover including chemo and radiotherapy

- Outpatient cover for consultations, specialist fees, physiotherapy and diagnostic tests like x-rays and blood tests

- Dental care

- Eye care

Other options

Of course, a traditional private medical insurance policy is not the only option for healthcare when you’re over 50.

NHS

This one goes almost without saying. The NHS is a prized and respected institution that looks after the majority of UK residents from cradle to grave.

It is important to bear in mind that if speedy appointments are your goal, then the NHS might not be the best option. Data from the end of March 2020 reveals that there were 4.24 million people on NHS waiting lists in England. More than one in five of these had been waiting for longer than 18 weeks.

However, it is likely that regardless of how comprehensive your private healthcare package is, it is likely that you will use the NHS in some capacity.

Self-funding

If you have the means, one option is self-funding your private healthcare. This means paying upfront for treatments, as and when you need them.

This can be achieved either with a single payment or by spreading the cost out with medical finance. Whilst this can be the cheaper route if you remain healthy, it can be a huge cost if you become unwell.

Continuation of a company policy

If your employer (prior to retirement) provided company health insurance, you might be able to continue the same policy in a personal capacity. These situations are rare though and talking it over with a trusted intermediary is the best option.

What to do next

- Do some thinking. Decide what you want from your policy and what you are hoping to achieve. Consider how much you are willing to spend as well, bearing in mind that prices are likely to rise each year.

- Speak to an impartial private medical insurance expert (like us!) and get some free advice. You will be able to ask questions and get a good idea of pricing and levels of cover. Try and find advisers who are independent and not tied to a single insurance company.

- Compare quotes. If you decide to purchase insurance through a broker or intermediary, they will provide you with several quotes you can choose from. With their help, you can decide which cover best suits your needs and budget. If you’ve changed your mind on anything, don’t be afraid of asking them to amend your quote.

- Choose your policy and apply.

- When the policy is confirmed, read through your policy documents and make sure you’re happy and understand everything.

Remember that your policy will renew each year on the same date and it will increase year on year. Lifepoint Healthcare carries out reviews each year to try and minimize these increases.

Can I get health insurance when I'm over 65?

Yes you can! It is relatively uncommon for people over 65 to purchase private medical insurance for the first time but it is possible.

However, that isn’t to say it will be simple or cheap. The price of cover is often the biggest point of concern. As price increases with age, the monthly premiums are nearly double what they are at 50.

Secondly, any pre-existing conditions won’t be covered by the policy. Of course, many conditions will appear prior to 65 years of age.

Finally, there are age limits with some insurers. Some won’t offer new policies to people above a certain age, which varies from 65 to 80+, depending on the insurer.

Measures like social distancing, frequent hand washing and mask-wearing should be employed to prevent the spread of COVID-19, regardless of the type of variant. The vaccine also greatly reduces the risk of becoming severely ill with all types of COVID variants.

Conclusion

Purchasing health insurance when you’re over 50 can seem like a big challenge, but the reality is very simple. It is mostly the same as purchasing an individual private medical insurance policy, regardless of your age.

…But there are a few additional factors – namely price – that are important to consider. The best way of approaching buying health insurance if you’re over 50 is to contact a trustworthy and impartial health insurance adviser who can talk you through your options.

Let's talk!

Because we know you have a busy day, let us know when would be a good time for you to talk.