This introduction is for individuals who are contemplating buying private medical insurance (PMI) for themselves or their families. We also have a free eBook called “An Essential Guide to Health Insurance for Companies” for those who are looking to invest in PMI for their employees.

It will be a general overview of the health insurance system in the UK. We will cover:

- What health insurance is

- What is and is not covered

- How to understand what you’re buying

- How it operates alongside the NHS

- How to use it

What is Private Medical Insurance?

Private medical insurance covers the individual for the cost of private medical treatment for acute conditions that begin after your policy has started.

An acute condition can be described as a disease, illness or injury that responds quickly to treatment that aims to return you to your previous state of good help, or help you make a full recovery.

Most private medical insurers will not cover chronic, or longer-term, conditions.

Chronic disease, injury or illness has one or more of these characteristics:

- It requires monitoring, control or relief of symptoms long-term

- It needs rehabilitation

- It may continue indefinitely

- It has a probability of return or no known cure

Private Health Insurance and the NHS

All customers who purchase PMI retain their right to use the NHS. The two systems are designed to work side by side.

It is common for PMI users to manage acute conditions that arise with their PMI and use the NHS for any chronic conditions e.g. diabetes. This is because the system is better designed for long-term management. It will also help to keep your premiums down long term.

Understanding What You’re Buying

There are many different choices when purchasing PMI. This includes:

- Type of treatment covered

- What cover level will apply to those treatments

- Where the treatment will be

- What contribution (excess) you will make

When considering purchasing PMI, you should consider:

- The benefits offered by each insurer

- Cover limits/monetary amounts

- Your personal health requirements

PMI, like any other insurance policy, is protecting something against future harm.

However, unlike other insurance policies, PMI represents significantly higher stales – after all, the “something” on the line is your or your families’ health, not a material object.

Purchasing PMI for the first time can be complicated, time consuming, and overwhelming, which is why we highly recommend enlisting the help of an independent adviser.

A health insurance broker can help you to save time and money, as well as help you to compare various policies and understand the ins-and-outs of your insurance. Learn more about how brokers/intermediaries can help you HERE.

NOTE:

Whilst private medical insurance and health insurance are sometimes used interchangeably, it’s important to note that health insurance can also refer to other types of insurance such as health cash plans, income protection and critical illness insurance.

How Private Medical Insurance Works

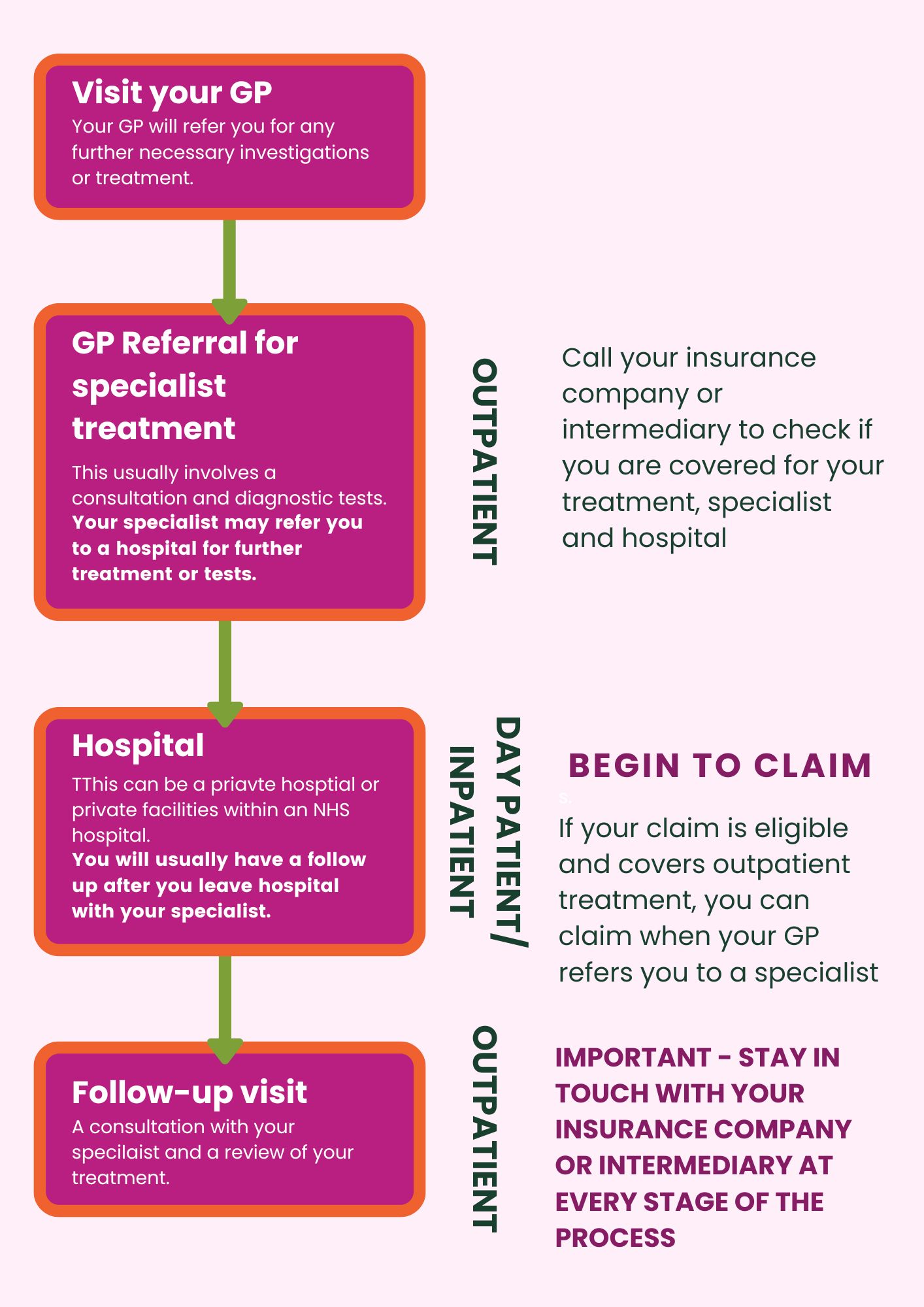

When you receive medical treatment in the UK, you will fall into one of three categories:

Outpatient

A patient attending a consultation, hospital or outpatient clinic without being admitted for treatment.

Day Patient

A patient admitted to a day patient unit or hospital for a period of medically supervised recovery without an overnight stay.

Inpatient

A patient who is admitted to hospital for treatment or observation and remains there for at least one night. This is usually the core cover for most private medical insurance policies.

The Process:

Though policies can differ, most private medical treatment starts the same way as it does on the NHS pathway – with a trip to the GP.

If required, the GP will refer you for specialist treatment. At this point, you can contact your insurance company who will check that you’re covered for the treatment.

It is a good idea to keep in touch with your insurer and broker at each stage of your treatment to ensure that you have guidance throughout the process. Some illnesses and their treatments will not be covered because they are pre-existing. Most of the time, you will already be aware of this when you are seeking treatment as pre-existing conditions should be discussed before you purchase your policy.

Here is an example of a potential pathway where you could claim on your private medical insurance:

Hopefully that has helped to clarify some points surrounding what health insurance is and how it works.

If you would like more information, give us a call now!

Share this article:

How to Choose the Right Health Insurance Policy (Step-by-Step)