The cost of health insurance is a bar to accessibility for many. This cannot be denied.

Price is also an important part of the buying process and it should be addressed honestly. This article will give you more information on how you should think about and approach the cost of your private medical insurance. This is true whether you are considering health insurance for the first time or your existing policy is coming up for renewal.

Hopefully it provides more clarity in making these important choices.

Price

Clients are rightly concerned about the rising costs of healthcare. Year on year, policies can increase by 10-20%, without any claims being made. When claims have been made, this can be far higher.

This makes it doubly important to know how to structure a plan when taking out a new policy as well as approaching your renewal.

Despite its undeniable importance, we believe that price shouldn’t be the absolute focus of the purchase. The issue of price tends to be a myth. Whilst as a buyer, you may want the lowest price, it is actually good value that you want.

When the value exceeds the price, then suddenly price no longer remains the issue. However, costs are still one of the biggest concerns for people and businesses when dealing with a premium product like private medical insurance.

The Make Up of a Health Insurance Policy

The cost of health insurance premiums Is affected by the benefits chosen for any given plan. Logically, the more comprehensive the level of cover, the higher the cost.

Policies tend to be modular.

This means that you start with a standard baseline of cover and can pick and choose additional benefits if you wish to enhance the cover level. This is where the policy can be “fleshed out” to maximise benefit and better personalise your policy.

This is where it is best to seek out the advice of an experienced professional to guide you on the myriad options available. A competent adviser would know all the options for each provider and how to structure the plan correctly to minimise cost and maximise benefit.

This is also why a price comparison site can never compare to an adept adviser. A real person can better listen to your needs and guide you towards your perfect fit.

Generalised Breakdown of Benefits

Each policy will have its own nuances of cover based on the following. Therefore, it’s always crucial to read the actual policy summary when considering a specific insurer and product.

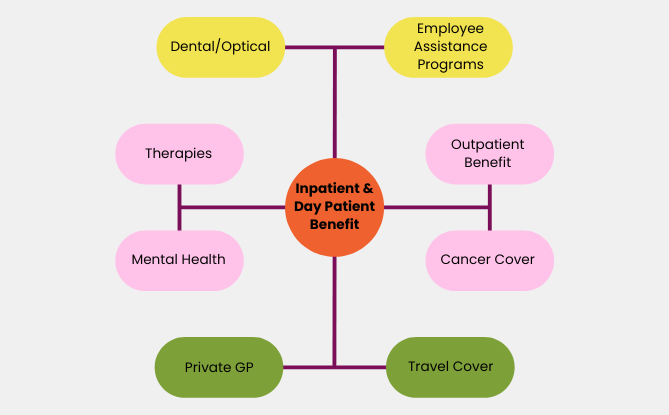

Inpatient and Day Patient Benefit

This relates to hospital charges for overnight stays and day cases.

This tends to be included as a baseline of core cover for most private medical insurance plans.

The cover may include: hospital charges including accommodation, meals, nursing care, drugs, surgical dressings, theatre fees, diagnostic tests, operating-theatre costs, radiotherapy, use of surgical appliances, and specialist fees for surgeons, anaesthetists and physicians.

Outpatient Benefit

This covers specialist consultations with approved specialists, diagnostic tests (including CT/PET/MRI scans/X-rays/blood tests/ECG’s), fees for practitioners. It might also include specialist referred physiotherapy, nurses, dieticians, orthoptists and speech therapists.

Cancer Cover

This may include the full cancer treatment pathways including: outpatient diagnostic tests and consultations, radiotherapy, chemotherapy and follow-up consultations, biological therapies, hormone and bisphosphonate therapies, cancer surgery and reconstructive surgery, stem cell therapy, and end-of-life home nursing.

NOTE

Given the cancer epidemic, we believe that cancer cover is a vital part of any health insurance plan. Life-saving treatment is incredibly costly and the peace of mind it provides is so important. The claims can be very high when treating cancer so full cover is required to ensure that most costs are covered.

Although most insurers now follow the trend of offering comprehensive cancer cover, there are some insurers that will have caveats. This means that its important to ask about the caveats before you take out your cover.

For example: Cancer caveats can vary from a limitation on how long a particular type of treatment may be given (biological therapies) or exclude certain treatments completely (bone marrow or stem cell transplants in certain situations).

Therapies

This may include fees for physiotherapy, acupuncture, homeopathy or therapist treatment, osteopathy, chiropody/podiatry, and speech and language therapy.

Mental Health

For treatment of an acute mental or psychiatric illness. This may include inpatient and day-patient treatment, outpatient treatment, psychologists, psychiatrists and cognitive behavioural therapists.

The mental health epidemic across the country worsens every year and the pandemic exacerbated it heavily. Mental health cover can be a prudent investment, none of us ever know when we’ll need it.

Fees can be incredibly costly without insurance in the private sector, whilst waiting lists on the NHS are so long that unless the case if life threatening, waiting over a year for talking therapies is commonplace.

Other

The above are the primary benefits available but there are a variety of additional extra benefits available depending on the insurer.

These can include:

- Dental and optical benefit

- Travel cover

- Private GP

- Employee assistance programs

- Extra membership benefits (discount schemes, free items, discounted gym memberships etc)

Levels of Cover

The levels of cover for some of the above can be further tailored depending on your needs.

For example: You can have a limitation on the use of the outpatient benefit – capped at a financial limit per year, or a maximum number of visits to a specialist. Or you could have a fully comprehensive benefit level which includes no annual limits.

Depending on which of the above benefits you choose, and at what level of cover, the plan and pricing can be tailored further, depending on the following:

Hospital Listings

Most insurers will have different levels of hospital listings which will affect the premium cost.

The most costly listing may cove all of the London hospitals. If you don’t require the inner London hospitals, and are happy with the hundreds of other options, then this is important to consider as a measure for cost containment.

Insurers do have different lists so it’s crucial to check that the list covers the facilities you would expect to use in a medical situation.

Level of excess chosen:

Generally, the higher the excess chosen, the lower the premium will be.

Excess amounts can range from £100 to £3000 with many variables in between. An excess can be payable per person per year or per claim (insurer dependent).

Or, it can be a co-payment option. Where you pay a percentage of the claim capped at an amount predefined at the time of policy set up.

Method of underwriting:

There are multiple methods of underwriting. Each poses a slightly different risk to the insurer so the choice of underwriting may also affect the premium.

Example: This is certainly the case when choosing Medical History Disregarded (MHD) as the insurer is aware that they’re more vulnerable to paying claims for pre-existing conditions.

Hopefully that has helped to clarify some points surrounding how health insurance can be structured and tailored to your individual needs.

If you would like more information, give us a call now!

Share this article:

How to Choose the Right Health Insurance Policy (Step-by-Step)