Table of Contents

How Does Private Health Insurance Cover Affect Your Tax?

Private medical insurance is highly valued by many employees. Faster access to diagnosis and treatment can support reduced absenteeism, improved morale, and greater loyalty.

From a business perspective, company private medical insurance may also be eligible for tax relief. However, there are tax implications for both employers and employees that must be understood and managed correctly.

Company Health Insurance and Tax FAQs

The information below is provided as general guidance only. Tax rules may change. For advice on specific circumstances, you should always speak to your tax adviser, accountant, or HM Revenue & Customs (HMRC).

Is a Limited company eligible for tax relief on a business healthcare plan?

Yes. If health cover is purchased through a Limited company, it is generally classed as a business expense and may be eligible for corporation tax relief.

I have a small, unincorporated business (not Limited). What are the tax implications if I provide health cover for my employees?

For unincorporated businesses, the cost of providing health cover for employees is deductible when calculating taxable profits. It is classed as a valid business expense and may qualify for tax relief.

Do I need to report company health cover to HMRC?

Yes.

At the end of each tax year, you must complete and submit a P11D form for each employee who has received the benefit.

You must also complete and submit a P11D(b) form and pay Class 1A National Insurance contributions on the value of the benefit provided.

As the owner of an unincorporated business, am I eligible for tax relief on a private healthcare plan for myself?

No. A private healthcare plan for yourself would generally be treated as a personal expense and would not normally qualify as a business expense.

Will employees need to pay tax on their private health cover benefit?

Yes.

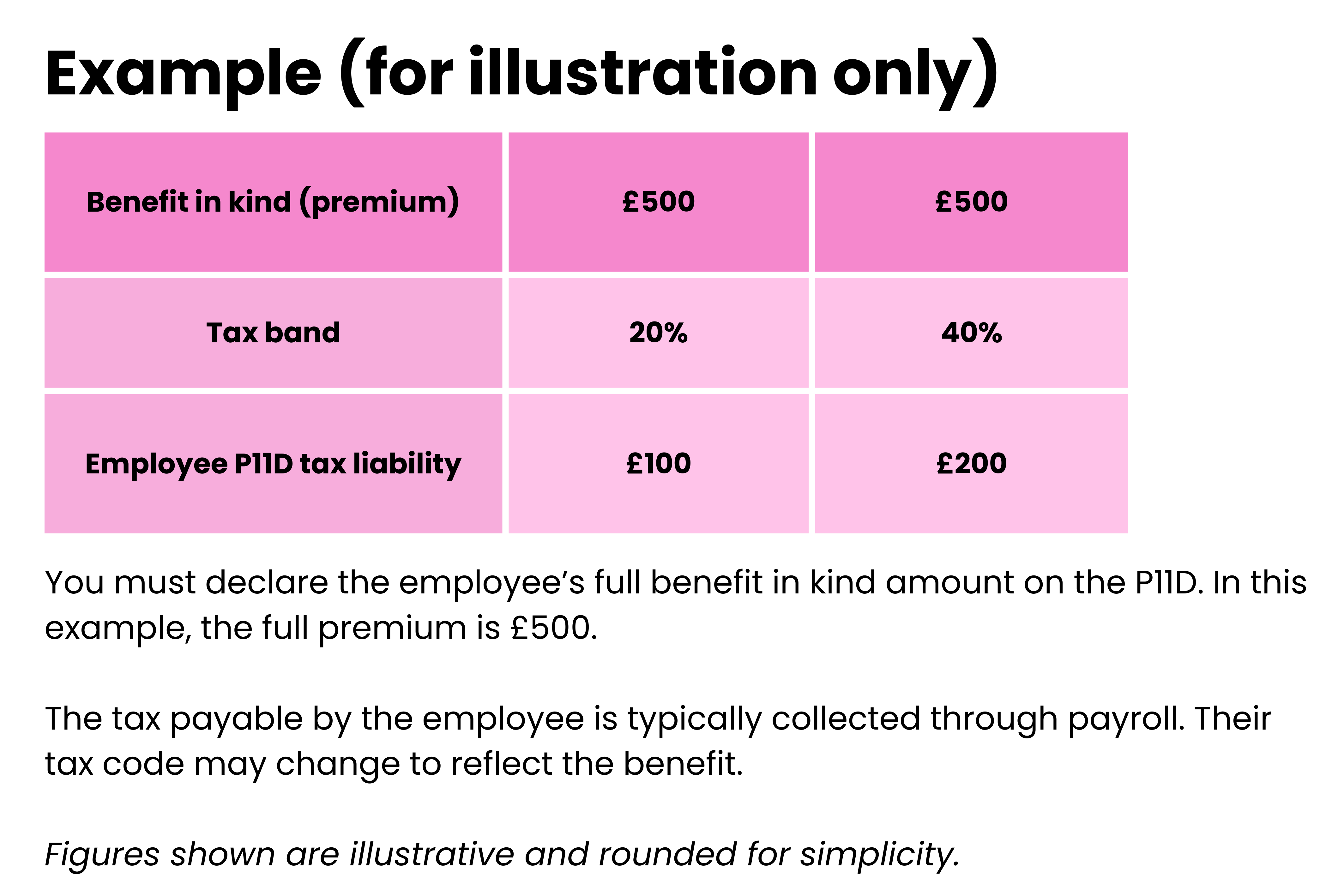

Employer-paid private medical insurance is considered a “benefit in kind”. Employees will usually need to pay income tax on the value of the benefit.

Is health cover subject to Insurance Premium Tax (IPT)?

Yes. Private medical insurance is subject to Insurance Premium Tax at the prevailing rate.

How Do I Calculate the Value of the Benefit in Kind?

The value of the benefit in kind is the employee’s private medical insurance premium.

Guide to Private Medical Insurance and P11D

The information below provides general guidance on handling private medical insurance when completing a P11D expenses and benefits form. For specific advice, always consult HMRC or your tax adviser.

What is a P11D?

A P11D (Expenses and Benefits Form) is issued by HMRC. At the end of each tax year, employers must complete a P11D for every employee or director who:

- Has received expenses or benefits in addition to their salary

- (Excluding routine business expenses such as travel or company car fuel)

Alternatively, employers can register with HMRC to payroll the benefit in kind voluntarily. Registration must be completed before the start of the relevant tax year.

Important Update

HMRC has announced that from April 2026, all taxable benefits, including private medical insurance, must be payrolled. P11D forms will no longer be available. Employers should review payroll processes in advance to ensure ongoing compliance.

What is the difference between a P11D and a P11D(b)?

- P11D: Reports expenses and benefits provided to employees.

- P11D(b): Reports the Class 1A National Insurance contributions due on those benefits.

Do you need to include private medical insurance on a P11D?

Yes.

When your company pays for an employee’s or director’s private medical insurance, it is treated as a benefit in kind and must be included on the P11D.

If the employee pays for their own policy personally, it does not need to be included.

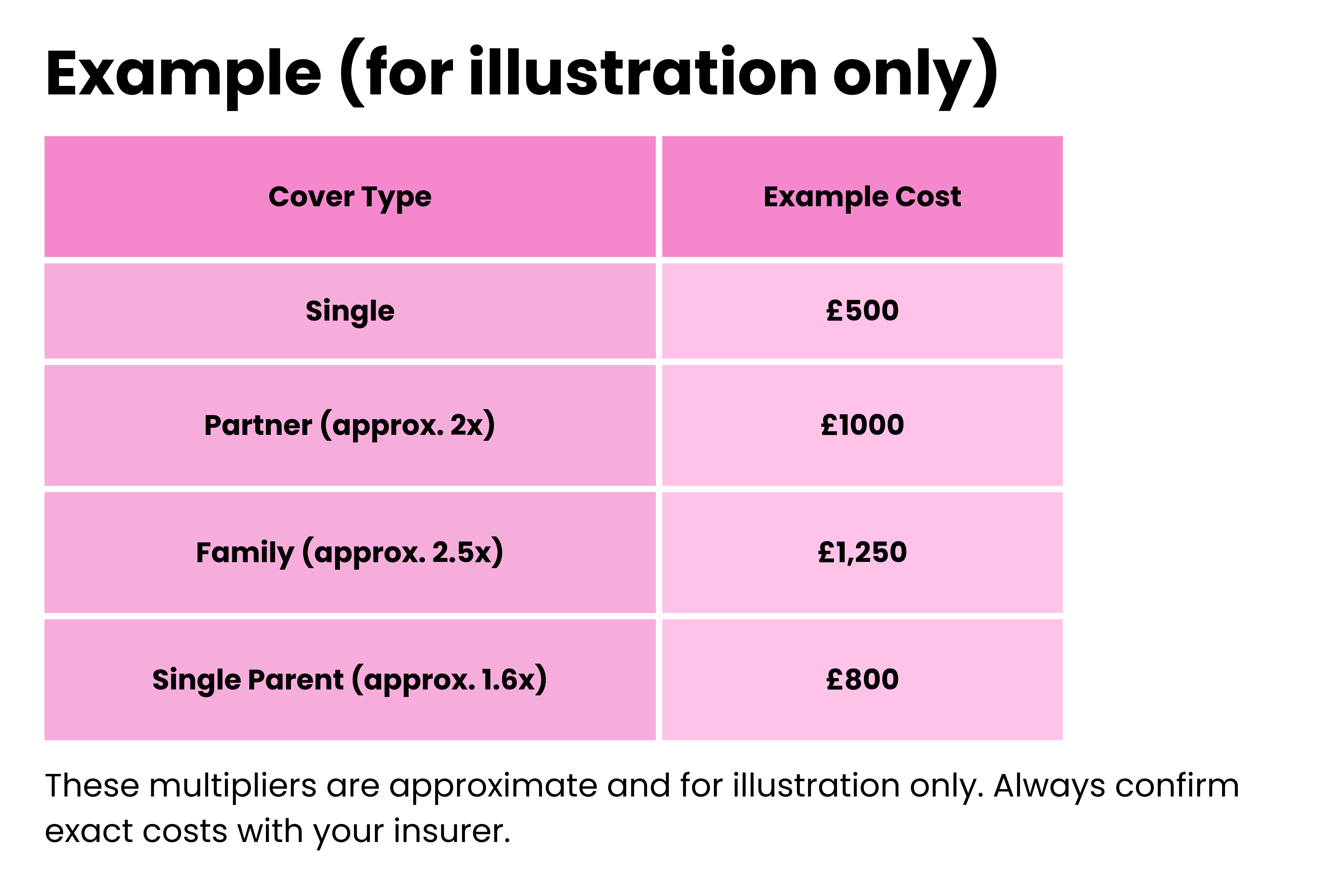

How do you know the cost per employee?

Your annual plan summary will show the cost of private medical insurance for each employee.

For example, if single cover costs £500:

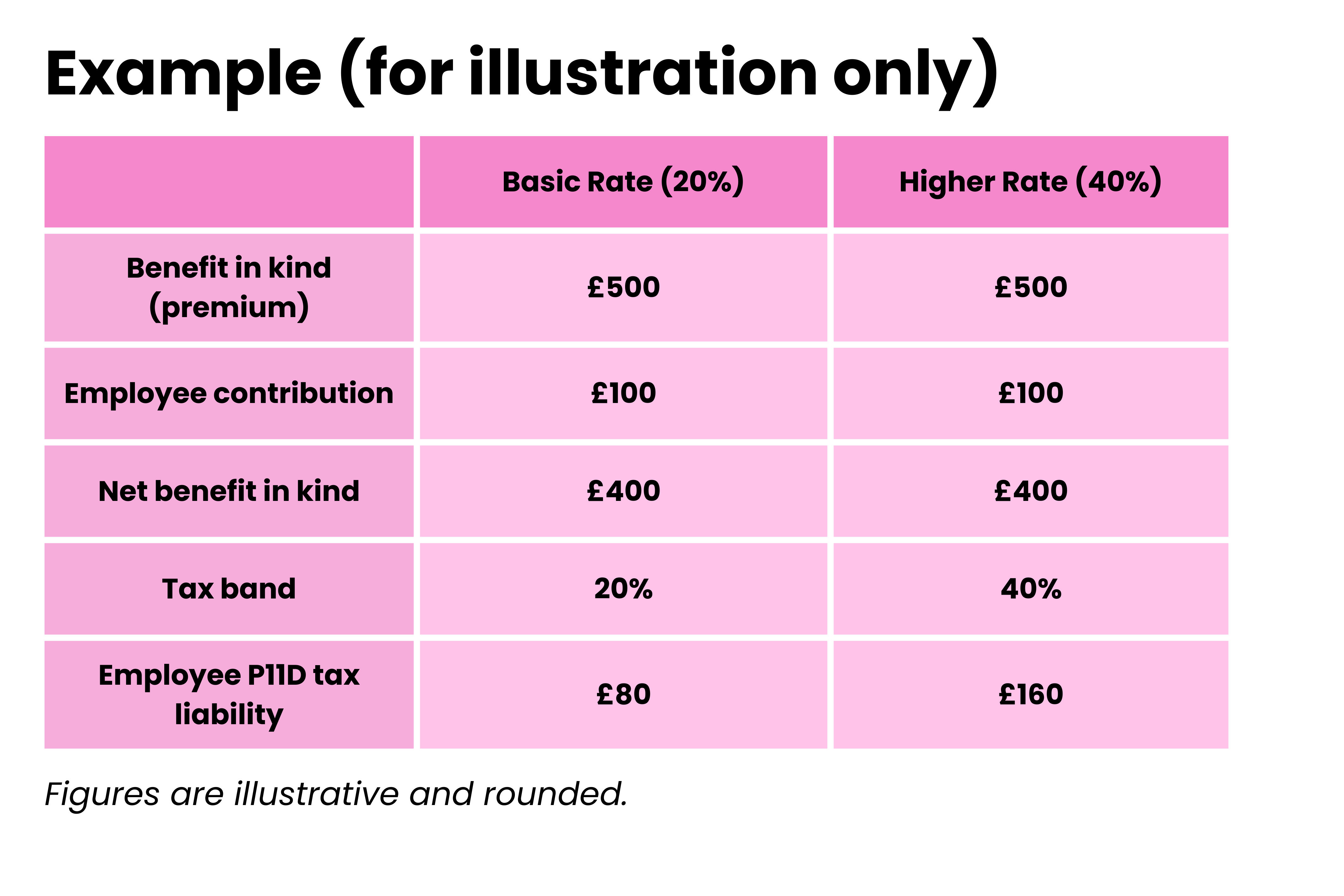

What if employees contribute towards the premium?

If an employee contributes to the cost, deduct their contribution from the total premium before calculating the benefit in kind.

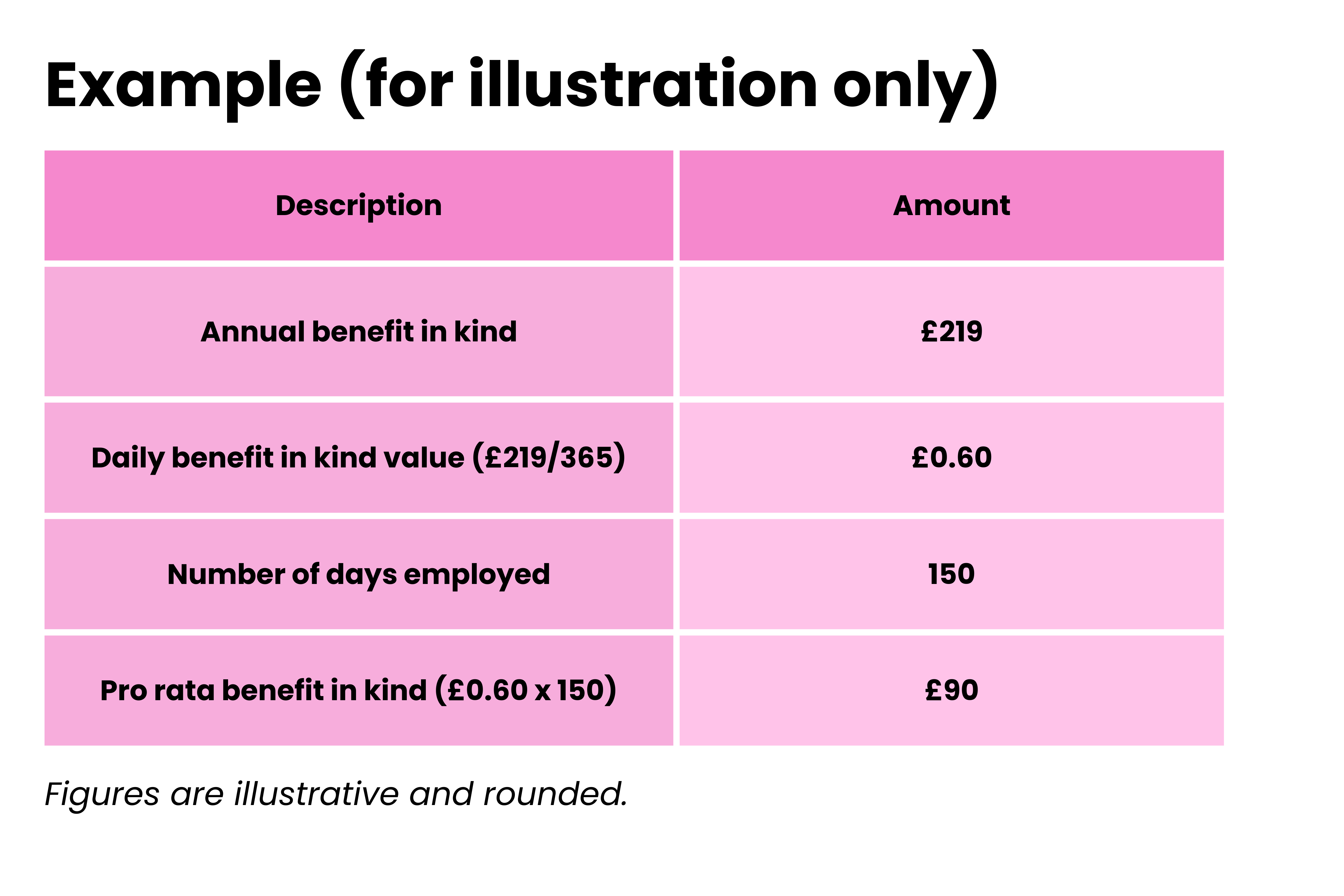

What if an employee joins or leaves part way through the year?

You must calculate the pro-rata value of the benefit for the period they were employed.

How Lifepoint Healthcare Can Help

We can assist by providing:

- Copies of your annual plan summary

- A breakdown of premiums per employee to support payroll reporting

- Liaison with insurers to request P11D reports where available

- General guidance to help you understand how private medical insurance is treated for tax purposes

Please note, we are not tax specialists. For specific tax advice, you should always consult your accountant or tax adviser.

If you would like support reviewing your company health insurance arrangements, please contact us to discuss your options.